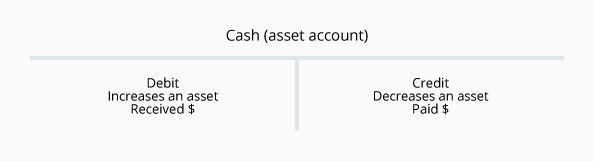

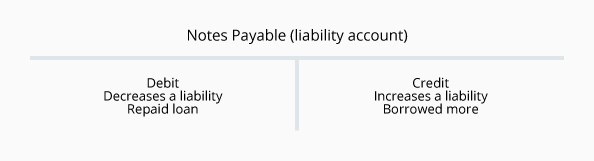

T-accounts

Accountants and bookkeepers often use T-accounts as a visual aid to see the effect of a transaction or journal entry on the two (or more) accounts involved.

To learn more about the role of bookkeepers and accountants, visit our topic Accounting Careers.

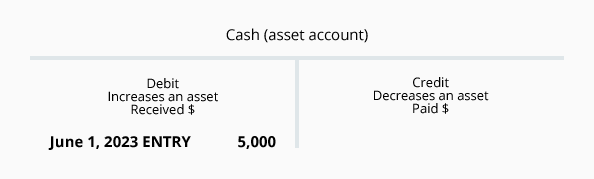

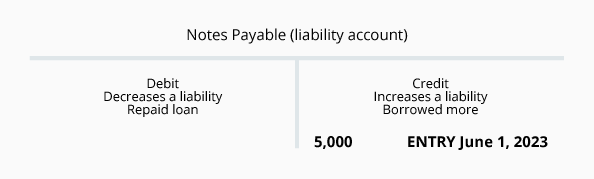

We will begin with two T-accounts: Cash and Notes Payable.

Let’s demonstrate the use of these T-accounts with two transactions:

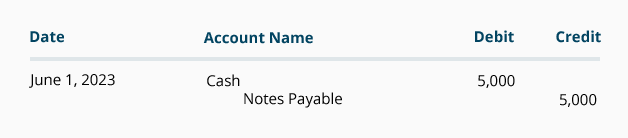

- On June 1, 2023 a company borrows $5,000 from its bank. As a result, the company’s asset Cash must be increased by $5,000 and its liability Notes Payable must be increased by $5,000. To increase the asset Cash the account needs to be debited. To increase the company’s liability Notes Payable this account needs to be credited. After entering the debits and credits the T-accounts look like this:

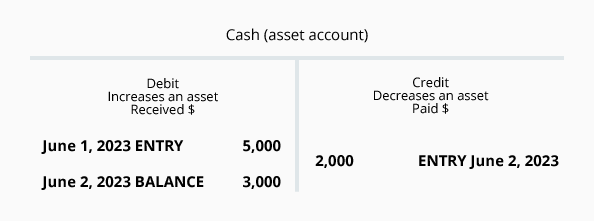

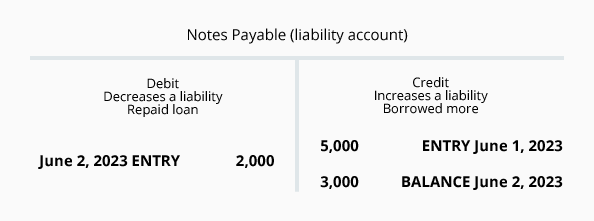

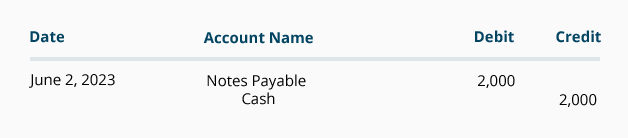

- On June 2, 2023 the company repays $2,000 of the bank loan. As a result, the company’s asset Cash must be decreased by $2,000 and its liability Notes Payable must be decreased by $2,000. To reduce the asset Cash the account will need to be credited for $2,000. To decrease the liability Notes Payable that account will need to be debited for $2,000. The T-accounts now look like this:

Please let us know how we can improve this explanation

No ThanksJournal Entries

Another way to visualize business transactions is to write a general journal entry. Each general journal entry lists the date, the account title(s) to be debited and the corresponding amount(s) followed by the account title(s) to be credited and the corresponding amount(s). The accounts to be credited are indented. Let’s illustrate the general journal entries for the two transactions that were shown in the T-accounts above.

Please let us know how we can improve this explanation

No ThanksWhen Cash Is Debited and Credited

Because cash is involved in many transactions, it is helpful to memorize the following:

- Whenever cash is received, debit Cash.

- Whenever cash is paid out, credit Cash.

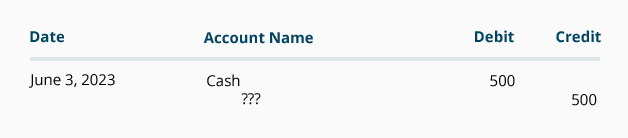

With the knowledge of what happens to the Cash account, the journal entry to record the debits and credits is easier. Let’s assume that a company receives $500 on June 3, 2023 from a customer who was given 30 days in which to pay. (In May the company had recorded the sale and an accounts receivable.) On June 3 the company will debit Cash, because cash was received. The amount of the debit and the credit is $500. Entering this information in the general journal format, we have:

All that remains to be entered is the name of the account to be credited. Since this was the collection of an account receivable, the credit should be Accounts Receivable. (Because the sale was already recorded in May, you cannot enter Sales again on June 3.)

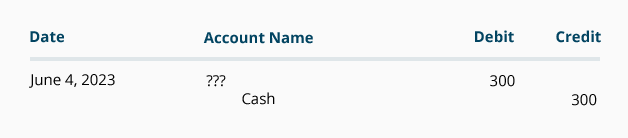

On June 4 the company paid $300 to a supplier for merchandise the company received in May. (In May the company recorded the purchase and the accounts payable.) On June 4 the company will credit Cash, because cash was paid. The amount of the debit and credit is $300. Entering them in the general journal format, we have:

All that remains to be entered is the name of the account to be debited. Since this was the payment on an account payable, the debit should be Accounts Payable. (Because the purchase was already recorded in May, you cannot enter Purchases or Inventory again on June 4.)

To help you become comfortable with the debits and credits in accounting, memorize the following tip:

Here’s a Tip

Whenever cash is received, the Cash account is debited (and another account is credited).

Whenever cash is paid out, the Cash account is credited (and another account is debited).

Please let us know how we can improve this explanation

No Thanks