Examples of Payroll Journal Entries For Salaries

NOTE: In the following examples we assume that the employee’s tax rate for Social Security is 6.2% and that the employer’s tax rate is 6.2%.

Let’s assume our company also has salaried employees who are paid semimonthly on the 15th and the last day of each month. The pay period for these employees is the half-month that ends on payday. There is one salaried employee in the warehouse department with a gross salary of $48,000 per year, or $2,000 per pay period. There are four salaried employees in the Selling & Administrative Department with combined salaries of $9,000 per pay period.

Because the salaried employees are paid on the last day of the month and their pay period ends on payday, there is no need to accrue for salaries at the end of December (or any other calendar month). The salaried payroll entry for the work period of December 16–31 will be dated December 31 and will look like this:

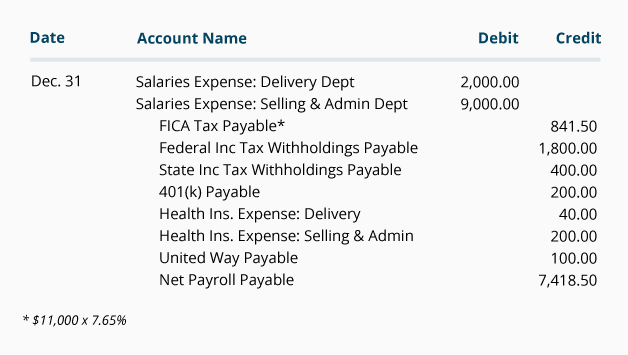

Salaried Payroll Entry #1: To record the salaries and withholdings for the work period of December 16–31 that will be paid on December 31.

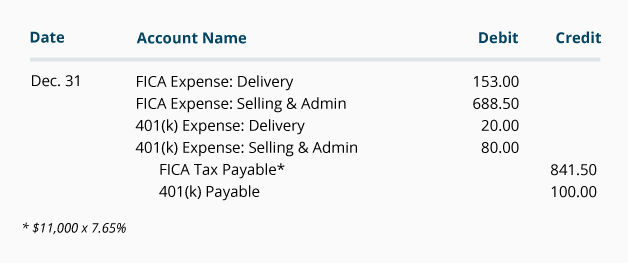

In addition to the salaries recorded above, the company has incurred additional expenses pertaining to the salaried payroll for this semi-monthly period of December 16–31. These expenses must be included in the December financial statements, as shown in the next journal entry:

Salaried Payroll Entry #2: To record additional payroll-related expenses for salaried employees for the work period of December 16–31.

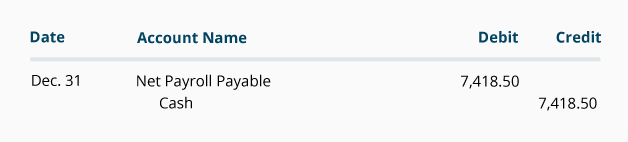

On payday, December 31, the checks will be distributed to the salaried employees. The following entry will record the issuance of those payroll checks.

Salaried Payroll Entry #3: To record the distribution of the salaried employees’ payroll checks on Dec. 31. (These checks reflect the take-home pay for the salaries earned during the work period of Dec. 16–31).

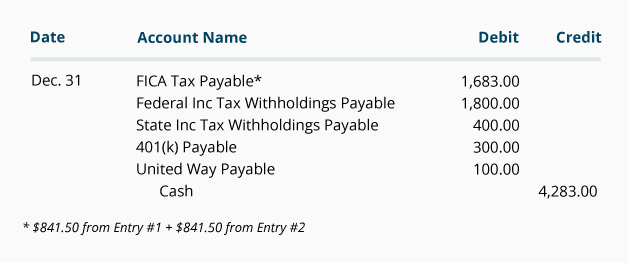

Some withholdings and the employer portion of FICA were remitted on payday; others are not due until a later date. Some withholdings, such as health insurance, were recorded as reductions of the company’s expenses in Salaried Payroll Entry #1. We will assume the amounts in the following Payroll Entry #4 were remitted on payday.

Salaried Payroll Entry #4: To record the remittance of some of the payroll withholdings and company matching that pertain to the salaried employees during the work period of Dec. 15–31.

Please let us know how we can improve this explanation

No ThanksWhen you join PRO Plus, you will receive lifetime access to all of our premium materials, as well as 12 different Certificates of Achievement.

Earn Our Certificate

for This Topic