Introduction to Bank Reconciliation

Did you know? You can earn our Bank Reconciliation Certificate of Achievement when you join PRO Plus. To help you master this topic and earn your certificate, you will also receive lifetime access to our premium bank reconciliation materials. These include our visual tutorial, flashcards, cheat sheet, quick tests, quick test with coaching, and more.

Earn Our Certificate

for This Topic

When you join PRO Plus, you will receive lifetime access to all of our premium materials, as well as 12 different Certificates of Achievement.

View PRO Plus FeaturesIn accounting, a company’s cash includes the money in its checking account(s). To safeguard this critical and tempting asset, a company should establish internal controls over its cash. These controls include separating the accounting duties of its employees, depositing all receipts into the company’s checking account, paying all bills through the checking account, and having an independent person routinely prepare a bank reconciliation (bank rec, bank statement reconciliation), and more.

The purpose of the bank reconciliation is to be certain that the company’s general ledger Cash account is complete and accurate. With the true cash balance reported in the Cash account, the company could prevent overdrawing its checking account or reporting the incorrect amount of cash on its balance sheet. The bank reconciliation also provides a way to detect potential errors in the bank’s records.

The bank reconciliation process requires some tedious tasks. For example,

-

Every check amount on the bank statement must be compared to the check amounts in the company’s general ledger Cash account. Any differences, such as the company’s outstanding checks and errors, will become part of the adjustments listed on the bank reconciliation.

-

Every deposit on the bank statement must be compared to the receipts recorded in the company’s Cash account. Any differences, such as a deposit in transit and/or errors, will become part of the adjustments listed on the bank reconciliation.

-

Other items on the bank statement must be compared to the other items in the company’s Cash account. Any differences, such as bank fees, checks returned because of insufficient funds, collections made by the bank, etc., will be part of the adjustments listed on the bank reconciliation.

The adjustments based on the above differences will be added or subtracted from one of the following amounts:

- The unadjusted balance from the bank statement (or online banking information)

- The unadjusted balance from the company’s general ledger Cash account

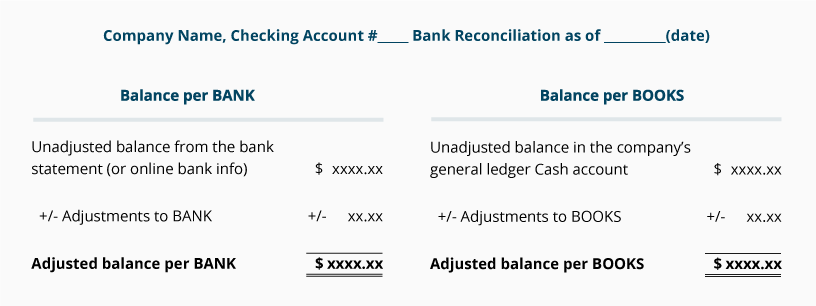

A condensed version of our format for the bank reconciliation is shown here:

Notice the following items in the condensed bank reconciliation format:

-

The left side is labeled Balance per BANK

-

The right side is labeled Balance per BOOKS

-

Adjustments to BANK (shown on the left side) are likely the items that are in the company’s general ledger Cash account, but they are not yet recorded in the bank’s records. Examples are outstanding checks and a deposit in transit. TIP: Put the item where it isn’t.

-

Adjustments to BOOKS (shown on the right side) are likely the items that the bank has recorded but the items are not yet recorded in the company’s general ledger Cash account. Examples include bank fees and a bank credit memo. TIP: Put the item where it isn’t.

-

If the amounts on the bottom line of the bank reconciliation are identical (Adjusted balance per Bank = Adjusted balance per BOOKS), the bank statement is reconciled.

-

In order for the adjusted balance (which is the true cash balance) to appear in the company’s general ledger Cash account and reported on the company’s balance sheet, the items listed under Adjustments to BOOKS must be recorded in the company’s general ledger accounts.

In the past, it was common for a company to prepare the bank reconciliation after receiving the monthly bank statement and before issuing the company’s balance sheets. However, with today’s online banking a company can prepare a bank reconciliation throughout the month (as well as at the end of the month). This allows the company to verify its checking account balance more frequently and to make any necessary corrections much sooner.

Please let us know how we can improve this explanation

No ThanksAccounting for Cash at the Company

It is helpful for a company to have a separate general ledger Cash account for each of its checking accounts. For instance, a company will have one Cash account for its main checking account, a second Cash account for its payroll checking account, and so on. For simplicity, our examples and discussion assume that the company has only one checking account with one general ledger account entitled Cash.

As you know, the balances in asset accounts are increased with a debit entry. Therefore, when a company receives money (currency, checks), the company debits its general ledger asset account Cash and credits another account using the date that the money was received (not the date the money is deposited at its bank). For example, if a company receives $900 on Saturday, June 29, the debit to the Cash account (and the credit to another account) will show the date of June 29, even if the money is deposited in the bank account on Tuesday, July 2.

When a company writes a check, the company’s general ledger Cash account is credited (and another account is debited) using the date of the check. Therefore, a check dated June 29 will be recorded in the company’s accounts using the date of June 29, even if the check clears (is paid through) the company’s bank account one week later.

The above transactions are common occurrences that illustrate two important points:

-

The unadjusted balance in the above company’s general ledger Cash account on June 30 is likely to be different from the bank statement balance on June 30.

-

Often, neither the June 30 unadjusted balance in the company’s Cash account nor the June 30 unadjusted balance on the bank statement is the true amount of the company’s cash. In that case, both unadjusted balances will need adjustments to arrive at the true, corrected, adjusted cash balance.

Next, we look at how a bank uses debit and credit when referring to a company’s checking account transactions.

Please let us know how we can improve this explanation

No ThanksAccounting at the Bank

To appreciate a bank’s use of the terms debit, debit memo, credit, and credit memo, let’s take a brief look at a few of the bank’s assets and liabilities:

- The bank’s assets include cash, investment securities, and loans receivable

- The bank’s largest liability is customers’ deposits

- Customers’ deposits consist of its customers’ checking accounts, savings accounts, and certificates of deposit

- Since customers’ accounts are liabilities of the bank, they will have credit balances

When a bank customer deposits $900 in its bank checking account, the bank’s asset Cash is increased with a debit entry, and the bank’s liability Customers’ Deposits is increased with a credit entry. The bank’s liability has increased because the bank has the liability/obligation to return the customer’s checking account balance to the customer on demand

When the bank increases a customer’s/depositor’s checking account balance, the banker might say that the depositor’s checking account was credited. (The credit entry does indeed increase both the depositor’s checking account balance and the bank’s liability.)

When the bank debits a depositor’s checking account, the depositor’s checking account balance and the bank’s liability to the customer/depositor are decreased.

Here are two examples to reinforce the bank’s use of debit and credit with regards to its customers’ checking accounts.

Bank Example 1. Assume that a new company opens a checking account at Community Bank with a deposit of $10,000. Community Bank records the deposit in the bank’s general ledger as follows:

- Debit of $10,000 to the bank’s asset account Cash

- Credit of $10,000 to the bank’s liability account Customers’ Deposits

Note that Community Bank credits its liability account Customers’ Deposits (which includes the individual depositor’s checking account balance). As a result, Community Bank’s balance sheet will report an additional $10,000 in assets and an additional $10,000 in liabilities.

Bank Example 2. Assume that a company pays its August rent of $1,000 by writing a check on August 1. Three days later, the landlord cashes the check at Community Bank. While the company had recorded the $1,000 check in its general ledger accounts with the date of August 1, Community Bank’s transaction occurs on August 4. Therefore, using the date of August 4, the bank will record this entry in the bank’s general ledger:

- Debit of $1,000 to the bank’s liability account Customers’ Deposits

- Credit of $1,000 to the bank’s asset account Cash

This transaction results in the bank’s assets decreasing by $1,000 and its liabilities decreasing by $1,000.

Please let us know how we can improve this explanation

No ThanksComparing Accounting: Bank vs. Company

Bank Example 1 showed that the bank credits the depositor’s checking account to increase the depositor’s checking account balance (since this is part of the bank’s liability Customers’ Deposits).

However, the depositor/customer/company debits its Cash account to increase its checking account balance.

Bank Example 2 showed that the bank debits the depositor’s checking account to decrease the checking account balance (since this is part of the bank’s liability Customers’ Deposits).

However, the depositor/customer/company credits its Cash account to decrease its checking account balance.

Please let us know how we can improve this explanation

No Thanks